It seems that the market has missed the significance of GGG’s latest ASX release.

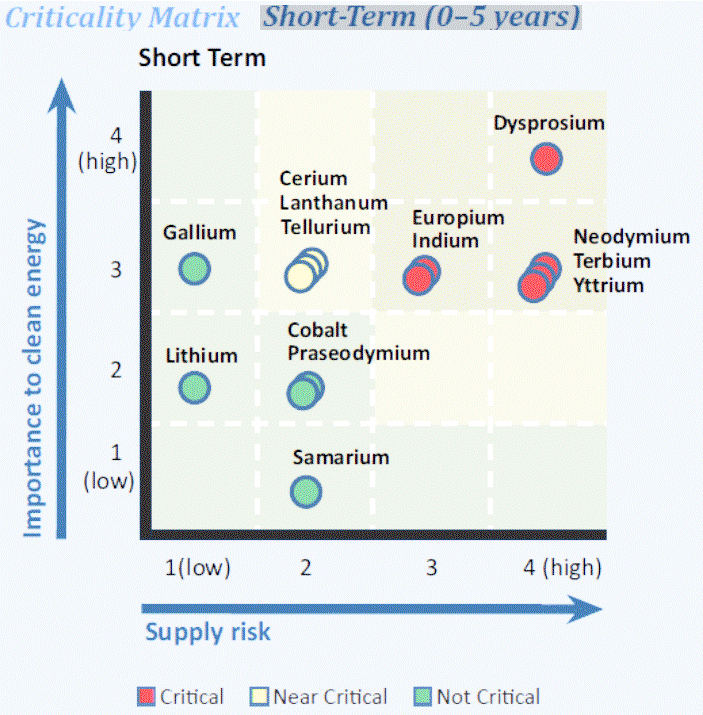

lately there has been a lot of commentary surrounding the impending surplus supply of REEs with several thousand projects around the world. The surplus is said to be coming in the light REEs whereas the heavy REEs are going towards critical supply shortage.

****And this is what the market seems to have missed:

CEO Rod McIllree

The resource base at Kvanefjeld is already very large, and initial resource calculations are due out for two new satellite deposits in early 2012. Given the advantage of having a very large resource base, our focus has been on establishing the most efficient and cost-effective way to process the material. We’ve also been conscious of identifying a development scenario with the least market risk.

The breakthrough in beneficiation provides a clear path to a more efficient operation, and also brings about greater flexibility: treating a higher-grade, lower-mass mineral concentrate opens up more leaching options than were previously available.

****We’re aiming for a primary leach stage that effectively leaches uranium and heavy REEs, and we’ve identified a number of solution chemistries to do this.

Under this scenario light REEs remain with the mineral residue, but in an easily leachable form.

****This would see Kvanefjeld developed as a uranium heavy REE project that also produces a very large light REE-rich stockpile. The stockpile can then be processed independently of the uranium-heavy REE leach circuit. Importantly, this removes the market risk of being dependant on producing, and having to sell a vast volume of light REEs, but leaves us the option of cheaply producing large volumes of light REE product according to demand.

This fits with our view that light REEs won’t retain their current high prices over the mid to long term, but heavy REEs will remain high-value materials of great strategic importance for many years to come. We aim to be a dominant supplier of heavy REEs and a large-scale producer of uranium oxide while retaining the option of cheaply producing a light REE product depending on market demand.

Thus it seems that GGG is positioning itself to become the world’s dominant supplier of heavy rare earths and a major uranium supplier.

I hold GGG.